Capital infusion from the group by way of preference capital has helped the company make progress on its debt restructuring programme, with interest costs cut by nearly half over the past couple of years. With more cash being released by recent exits from non-core businesses, there appears to be further scope for interest cost savings from a continuation of debt restructuring efforts.

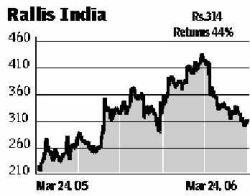

After registering a robust 80 per cent growth in post-tax profit on the back of a 15 per cent sales growth in the first half of this fiscal, Rallis has received a sharp setback to both revenues and profit in the December quarter.

However, investors in agrochemical stocks have to be prepared for volatile earnings as they depend on only on the state of agricultural output, but also on pest incidence in a particular season, which is always a wild card.

However, the modest valuation multiple enjoyed by the Rallis India stock may make it more resilient to downside.